We need warnings labels for home equity lines of credit.

HELOCs are like drugs – helpful to many and dangerous or even addictive to a significant minority. A survey to be issued Tuesday by the Financial Consumer Agency of Canada (FCAC) highlights the dangers.

The survey included about 4,800 people, 26 per cent of whom had a HELOC. Of this group, roughly one in four had a timeline for repaying what they owe that ranged from five years to never. A little more than one-quarter always or mostly make only the minimum monthly maintenance payment of interest every month and thus don’t pay down their principal.

Saddest of all: Thirteen per cent of HELOC holders in the survey said they frequently used their credit line to meet payments on other debt, such as a mortgage or credit card, and another 16 per cent said they sometimes did this.

A lot of holders deserve kudos for using their credit lines correctly – as a low-cost way to borrow money you can afford to pay back in the near to medium term. But the survey clearly shows that a strong minority of people are doing harm to themselves. Their credit lines have turned into perma-debt and a source of funds to meet household expenses.

The FCAC, a federal agency, has been digging into HELOCs over the past couple of years because they’re the most common form of consumer debt after mortgages. HELOCs are secured by the equity in your home, so they offer interest rates that are much lower than loans or unsecured credit lines. You typically have the option of paying just the interest owing every month, so there’s a lot of repayment flexibility.

The FCAC survey included nine questions about how they work – just three questions were answered correctly on average by all participants, while those who had one nailed four questions. The FCAC is definitely on the mark in its goal of working with banks and other lenders to improve disclosure of terms and conditions.

There were about 3.1 million HELOCs in Canada as of early 2018, according to Canada Mortgage and Housing Corp. Among the two-thirds of them in use, the average balance owing was $97,000.

The big risk with HELOCs is that people get themselves into debt and can’t get out. In the FCAC survey, 27 per cent of holders were making interest-only payments mostly or every month. Among holders aged 25 to 34, 41 per cent were in this category.

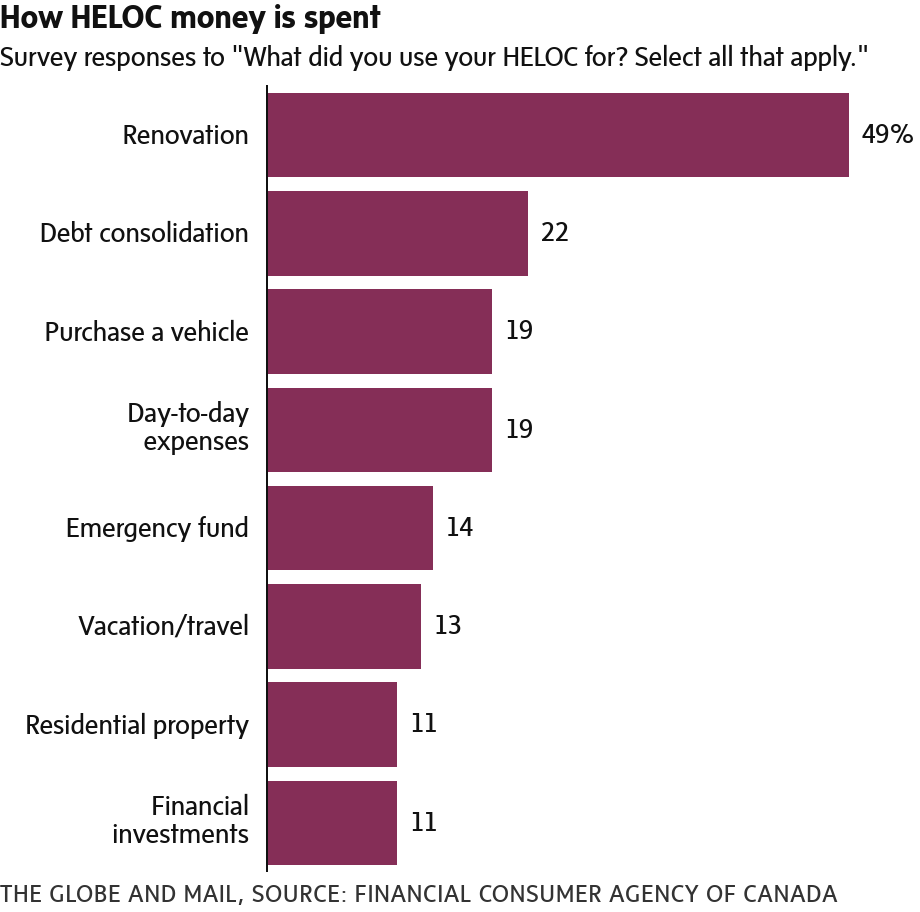

You can see HELOCs going sideways in the 19 per cent of people who borrowed more than they intended. How does this happen? The answer may be found in the fact that nearly half of holders in the survey borrowed money for home renovations. HELOCs are a natural way to pay for a renovation, but they’re not to be treated as a blank cheque.

Just more than 40 per cent of HELOC holders in the survey said they borrowed as much as they thought they would at the start, and 19 per cent had not yet used their credit line. Kudos to that latter group – they have a powerful borrowing tool at their disposal, but have the discipline not to use it.

In fact, many people deserve good grades for the way they handle their credit line. One-third of HELOC holders in the FCAC survey said they planned to pay off their debt in less than one year. An A-plus for these people.

Another 28 per cent of holders had a timeline of one to five years – two or three years is good, four or five is pushing it. Among the rest of the survey participants, 13 per cent said they didn’t know when they would pay off their debt, 14 per cent said five to 10 years, 10 per cent said more than 10 years and 2 per cent said never.

A warning label for HELOCs might simply say this: “Use responsibly. If you can’t pay the money back fully in one to three years, this product isn’t for you. Harmful effects from misuse include chronic indebtedness.”

ROB CARRICK

PERSONAL FINANCE COLUMNIST

The Globe and Mail, January 15, 2019