During the pandemic, households have saved a lot more cash than usual. Where it’s spent – and how quickly – carries big implications for the economy.

Paul Bannister is making up for lost time.

He has just returned from 10 days of “island hopping” in the Bahamas with his wife and kids, a longer vacation than he’d normally take. Back home in Pickering, Ont., just east of Toronto, the family often goes out to pricey restaurants – steak dinners are a popular choice – no matter the sticker shock on menus.

A semi-retired business consultant, Mr. Bannister watched his expenses plummet in the early stages of the pandemic, leaving him with extra cash. But after months of looser public-health measures, he reckons he has spent those savings and then some, eager to reclaim a semblance of normalcy. “We weren’t able to go anywhere for two years,” he explained. When he spends now, his mentality is “let’s make the experience much more enjoyable.”

Like Mr. Bannister, many Canadians amassed exceptionally large amounts of savings during the pandemic. The countrywide total is a hefty – and somewhat mysterious – sum of money that continues to grow. Some of Canada’s major banks have pegged excess savings over the past two years – that is, savings above typical levels – at roughly $300-billion.

No doubt, that money comes with far-reaching implications for the economy. Deputy Prime Minister Chrystia Freeland has referred to savings as “preloaded stimulus” to power the country’s economic recovery. Troubled service industries, such as tourism and restaurants, are counting on a summer surge of revenue after a brutal period of meagre sales.

But there’s a difference between excess savings and available cash. The latter sum is much smaller. After all, people have put large chunks of their savings to work in various ways. Some of the money has gone toward reducing non-mortgage debt, some toward homes that have soared in price, and some toward stocks that, until recently, were also riding a dizzying rally.

Where the leftover money will be spent, and how quickly, is anyone’s guess. The Bank of Canada estimates that $40-billion in excess savings will be spent by the end of 2024, but doesn’t attach much confidence to that forecast. There is undeniable upside to higher spending, but also risk. For instance, if Canadians splash out in the coming months, that could give an unhelpful boost to inflation, already running at a three-decade high.

The flip side is that excess cash could turn into scared money. Canadians are more indebted than ever, and with borrowing rates on a rapid climb, debt-servicing costs are becoming more onerous. The average worker is seeing their wages tumble, after accounting for the corrosive effects of inflation. And two of the major drivers of wealth over the pandemic – stocks and real estate – are now mired in a slump.

Shannon Lee Simmons, a certified financial planner in Toronto, has noticed a shift among her clients. In 2021, it was all about using savings to buy stocks, pay for home renovations or get into more speculative areas, such as cryptocurrencies or day trading. Now, she said, people want a cushion against rising financial risks.

“Last year, I really felt like I was having conversations about spending money,” she said. “Now that we’re almost midway through 2022, I’ve seen the erosion of a lot of those really stacked emergency accounts.”

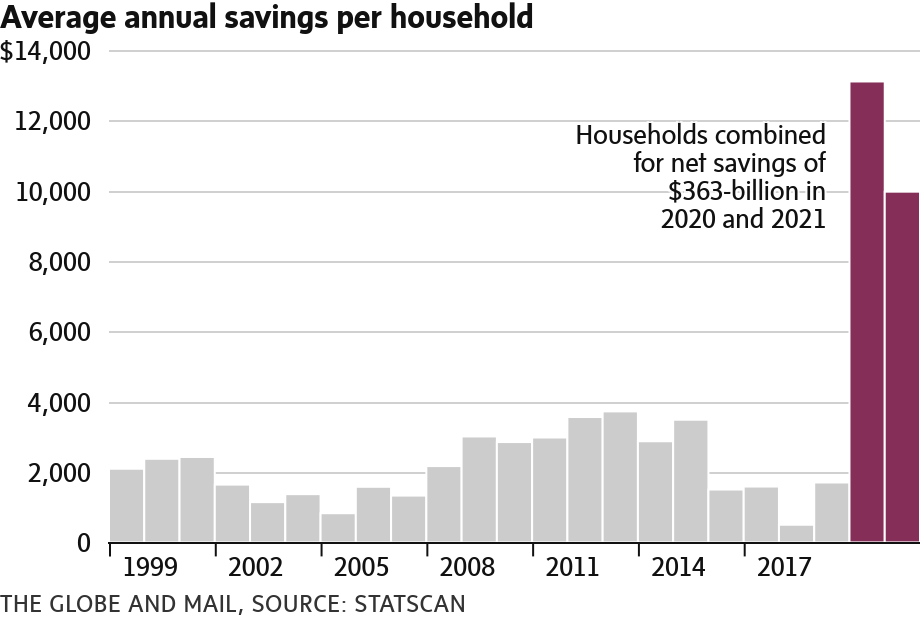

Heading into the pandemic, Canadians weren’t exactly big savers.

The savings rate – that is, the country’s total savings as a percentage of disposable income – had been declining for decades, and in 2018 the average household socked away just $500, down from about $3,700 in 2013.

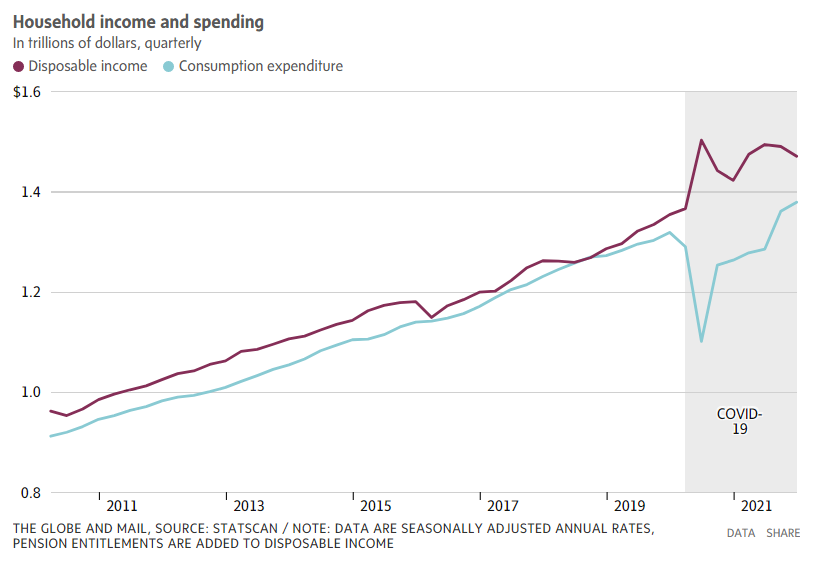

Then the pandemic arrived, delivering a shock to balance sheets. Disposable income jumped, owing to COVID-19 financial assistance from the federal government that exceeded the loss of wages, while consumer spending fell substantially amid lengthy lockdowns.

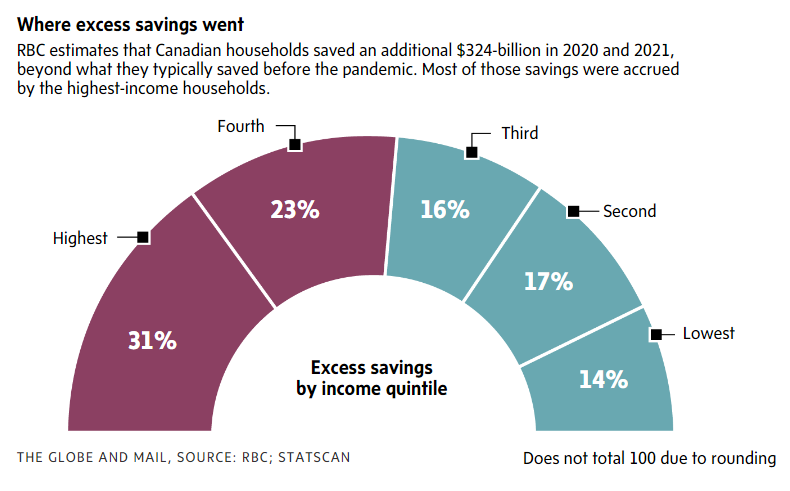

Those twin factors coalesced to send savings skyward. In 2020 and 2021, household net savings totalled about $363-billion. Royal Bank of Canada estimates that $324-billion of that was in excess of typical sums.

Just about every Canadian was thrust into a forced savings plan, which, for some, was a welcome reprieve from cumbersome expenses. In a range of demographic groups – the young and the old, the low and highly paid, renters and homeowners – net savings have improved.

But like so many aspects of the pandemic, the spoils weren’t shared evenly. Out of the excess savings, about 31 per cent accrued to the top 20 per cent of households by income, but only 14 per cent to the bottom fifth.

Moreover, any notion that $324-billion is just waiting on the sidelines, ready to supercharge the reopening, is simply misguided. Statistics Canada calculates savings before the purchase of wealth-generating assets, such as homes, renovations and mutual funds – all areas of big spending over the past two years.

“I think it’s fair to say that it’s not necessarily like $300-billion is sitting there in a chequing account, waiting to be withdrawn,” said Matthew Hoffarth, a section chief at Statscan.

Benjamin Tal, deputy chief economist at CIBC Capital Markets, estimates there is around $90-billion in excess deposits. That’s about 1½ months’ worth of retail spending in Canada. And he suspects that money is largely residing in the accounts of middle-to-high-income individuals.

“Their propensity to spend on leisure and services is much higher. Therefore, the contribution to the economy from that spending will be more significant because that’s where we’re opening up,” he said.

There’s a paradox in the excess savings Canadians have built up. On the one hand, they could support spending as consumer prices and borrowing costs rise. On the other hand, extra money sitting in bank accounts could add to inflation, forcing the central bank to act more aggressively.

“It’s a bit of a double-edged sword,” said Sal Guatieri, a senior economist at Bank of Montreal. “Not only is it supporting spending, it’s supporting inflation as well, as people in both the U.S. and in Canada have been a little more willing to pay more, pay higher costs, given that cash cushion.”

This puts the Bank of Canada in a delicate position. It needs robust consumption growth to prevent the economy from slipping into recession as interest rates rise sharply. But too much consumer spending – particularly on durable goods that are still constrained by gummed-up supply chains – could make the inflation-control job more difficult.

The central bank is betting that consumers start buying fewer couches, bikes and electronic devices and start spending on restaurants, vacations and other services that were curtailed during the pandemic lockdowns. This shift in demand could help cool consumer-goods inflation, which has accounted for a disproportionate amount of overall inflation relative to services. But changes to consumer spending are hardly a sure thing.

“We think that, as things reopen, the growth in demand for goods will slow down and the growth in demand for services will go up. But given that they have these extra savings, yes, you could see strong growth continue in both,” Bank governor Tiff Macklem said in a Senate committee appearance in February. “That would give us even stronger growth than we have got as a projection. Other things equal, that would mean that interest rates would likely have to go up more to dampen spending and bring it down in line with supply.”

In a world of steep inflation and rising rates, low-income households are particularly vulnerable. A greater proportion of their budgets is dedicated to everyday necessities, such as groceries and rent, both of which are escalating in price. And those households face steeper debt payments, as a proportion of disposable income. With fewer savings on hand – and presumably, for some people, none at all – the coming years could be tough to manage financially.

“Those that already had savings accumulated a lot more savings. Those that didn’t have savings didn’t really see that much of a change,” said Clayton Buckingham, chief financial officer of Vancity, Canada’s largest credit union, which operates in British Columbia.

Lower-income households, he said, “didn’t have a lot of money going into this, and now they’re likely to be more impacted by the impacts of inflation, particularly given that it’s really focused on gas, food prices.”

On average, Vancity clients have around $3,000 more in their deposit accounts than before the pandemic, Mr. Buckingham said. And those savings keep piling up: Clients have added around $1,000 more since the start of the year.

But those savings could be eroded quickly by the combination of inflation and higher interest rates.

“I do think it will provide some buffer, but if we don’t see wages rise commensurate with inflation, then we’re simply going to see that get eaten away and then the pressure will really start to hit,” he said.

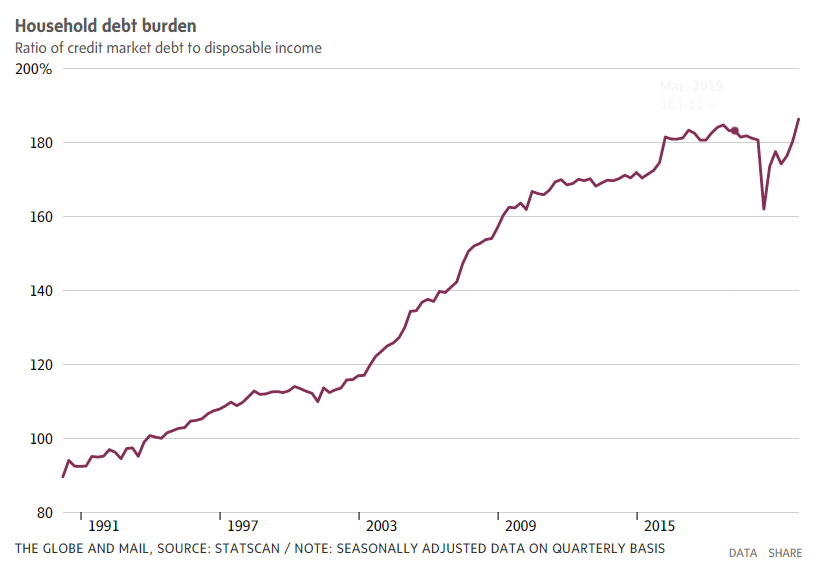

The growth of savings is only half the story. On the other side of the ledger, household debt ballooned during the pandemic. Canadians used some of their extra savings to pay down credit cards and lines of credit. But they also gorged on real estate, adding more than twice as much mortgage debt in 2021 as in 2019.

By the end of 2021, Canadians owed a record $1.86 for every $1 of disposable income.

Because mortgages were taken out or renewed at near-zero interest rates, the cost of servicing this mountain of debt remains below the previous peak in 2019. That could change fast as interest rates rise. Michael Davenport, an economist with Oxford Economics, expects household interest payments as a share of disposable income will surpass the 2019 peak by the middle of next year.

“Higher interest rates are going to eat into household spending, primarily through higher borrowing costs. And so what you’re going to see is that households will not have as much money to spend on discretionary consumer goods and services,” he said.

As with savings, the household debt story is more complicated than the aggregate numbers suggest. The majority of Canadian households have fixed-rate mortgages, so they won’t feel the pinch of higher rates until they renew. Likewise, many variable-rate mortgages have fixed payments, which means mortgage holders won’t face a sudden jump in monthly expenses as the prime rate increases – although they will have to pay more in interest and less toward principal each month.

These mitigating factors do not mean Canada’s mortgage market has a clean bill of health heading into an aggressive rate-hike cycle. In November, Bank of Canada deputy governor Paul Beaudry gave a speech warning about the rising proportion of highly indebted households and the growing number of new mortgages issued with extremely high loan-to-income ratios.

He also said that the rising proportion of real estate investors – who now account for around one-fifth of home purchases – may increase the probability of a housing-market correction. Real estate investors tend to have higher debt-service ratios than non-investors and could be more eager to sell in the face of rising rates or the loss of income.

“High debt levels mean the economy could react particularly badly to certain types of shocks, especially ones that affect income and house prices or cause interest rates to rise substantially,” Mr. Beaudry said.

The Bank of Canada has embarked on its quickest pace of monetary-policy tightening in decades, taking the benchmark interest rate to 1 per cent, with several more hikes on the way. Already, this era of tighter borrowing conditions has sent a shudder through the housing market, with a quick pullback in sales.

The picture is generally better on the consumer debt side of things. Consumers used their excess savings to pay down high-interest debt, and delinquency and default rates on things such as credit cards and lines of credit fell during the pandemic.

Delinquency rates are starting to creep back up, although they remain below prepandemic levels, said Matthew Fabian, director of financial services research and consulting at the credit reporting agency TransUnion.

TransUnion estimates that around 10 per cent of credit users typically face some strain on their ability to meet minimum payments as interest rates rise.

“That’s not to say that they’re all going to go delinquent,” Mr. Fabian said. “For some of them, it’s just, ‘Hey, I can’t go to Starbucks every morning any more, I can’t go to the Keg on Friday.’ You have to make trade-offs.”

This rate-hike cycle, however, could hit people harder than previous cycles, he said.

“There’s going to be a period where inflation still remains high, but interest rates also are high. So now you have less disposable income to start with to allocate toward paying down debt, but the debt that you have is also more expensive. And until one kind of fully offsets the other, there’s going to be a small pocket of people that are going to be hit on both sides,” he said.

Stocks are another source of recent pain. Ms. Simmons, the financial planner, saw all sorts of potentially risky behaviour when markets were surging and the likes of GameStop Corp. and dogecoin became household names thanks to enthusiastic, and sometimes novice, retail investors. “It’s absolutely shocking the skyrocketing amounts of day trades, of crypto trades, of [non-fungible token] trades, and the amount of losses and risks that some people took,” she said. “Oh my goodness.”

After a buoyant 2021, she’s often having difficult conversations with clients this year, telling some to avoid purchases of big-ticket items and build a financial buffer. She senses that clients are getting nervous, “especially if they have stretched the limits of what they were able to do through borrowing.”

Kashyap Arora is taking a more prudent approach to his finances than some. A quantitative analyst, he moved to Toronto from India just as the pandemic was hitting Canada. He has been able to save around $20,000, which he plans to split between an emergency fund and purchasing exchange-traded funds.

“If I was living with family, it would have been a bit different. But since I’m living alone, I’m the only one earning, so yeah, I’ve been very responsible,” he said.

In the fourth quarter of 2021, the savings rate hit 6.4 per cent, the lowest point during the pandemic – but still much higher than the quarterly average of 3.4 per cent during the 2010s. The consensus on Bay Street is that the rate will drop further.

CIBC’s Mr. Tal expects households to save less as they ramp up spending and absorb higher costs. In that scenario, people could buy more, but leave their excess deposits untouched.

That could prove useful for a rainy day.

MATT LUNDY, ECONOMICS REPORTER

MARK RENDELL

The Globe and Mail, May 13, 2022