Canadian households’ debt loads rose to another record high in the third quarter, as mortgage debt continued to climb despite rising interest rates.

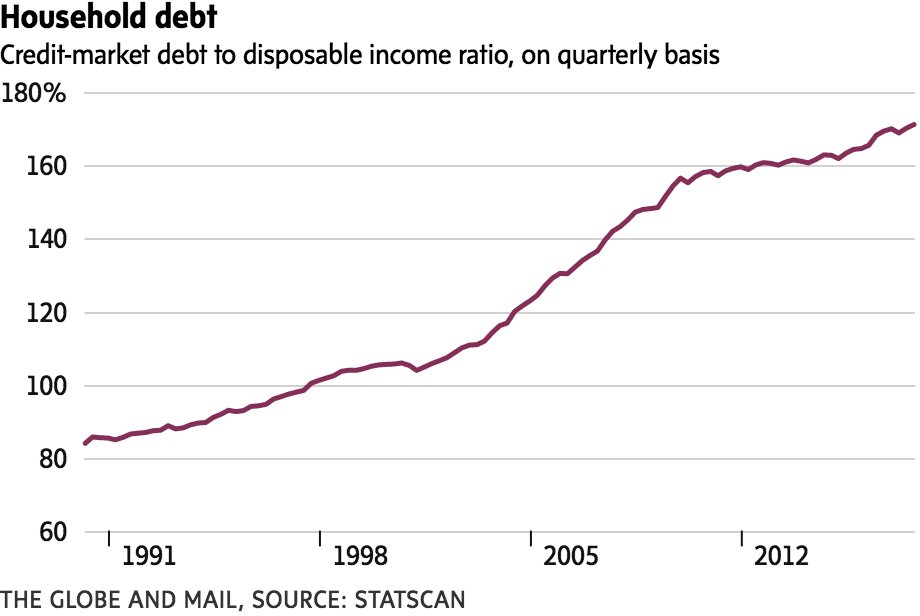

Statistics Canada reported that the ratio of household credit-market debt to disposable income – the key gauge for measuring Canadians’ debt loads – rose to 171.1 per cent in the three months ended Sept. 30, up from a revised 170.1 per cent in the second quarter (originally reported as 167.8 per cent).

Total household credit-market debt increased 1.4 per cent in the quarter, to $2.11-trillion, also a record. Credit-market debt is made up of mortgages, consumer credit (such as credit cards and lines of credit), and non-mortgage loans.

The report will be a source of concern for the Bank of Canada, which considers the country’s high household debt levels to be the biggest source of vulnerability for country’s economic outlook and financial-system stability. After an encouraging flattening of the debt-to-income ratio a couple of years ago, the ratio surged again last year and has hit record highs the past two quarters.

“Today’s household debt numbers told a familiar story as borrowing once again outpaced disposable income growth,” said Royal Bank of Canada economist Josh Nye in a research report.

Statscan said the main contributor to the increase was mortgage debt, which grew by 1.5 per cent in the quarter, to $1.38-trillion. Borrowing continued to climb despite rising interest rates on mortgages, as the Bank of Canada raised its key rate twice during the quarter, by a total of half a percentage point.

The rise in mortgage borrowing also came despite evidence of a cooling in some of Canada’s key housing markets, particularly the Toronto market. The Canadian Real Estate Association’s home price index declined nearly 2.5 per cent in the quarter.

But economists believe some home buyers may have jumped into the market to take advantage of preapproved mortgages on which the interest rates were set before the rate increases, and to lock in before regulatory changes take effect that will toughen mortgage borrowing requirements.

“With home buyers rushing to get into the market ahead of the new [Office of the Superintendent of Financial Institutions] rule change that takes effect on Jan. 1, 2018, we could see a further increase in the fourth quarter,” said Bank of Montreal economist Benjamin Reitzes in a research note.

While borrowing continues to climb, Canadians’ household net worth dipped 0.1 per cent in the quarter, a function of the pullback in housing prices. Statscan said residential real estate values suffered their first quarter-to-quarter consecutive decline since 2009.

“We are concerned that a growing number of Canadians will put themselves at risk and be unable to maintain their household expenses and reduce debt levels in the future,” said Scott Hannah, president of the Credit Counselling Society, in a statement released in response to the Statscan report.

But with the new mortgage rules coming in next year, interest rates rising and key housing markets already cooling, economists are optimistic that the household debt trend will start improving in 2018.

“The rising cost of borrowing, and more reasonable trends in home prices, should slow credit growth in the years ahead. And with incomes expected to continue increasing, the trend in debt-to-income should flatten out – a development policy-makers are keen to see,” Mr. Nye said. “But even if that dynamic plays out, households will remain stuck with high debt loads – keeping financial system vulnerabilities elevated in the years to come.”

DAVID PARKINSON

ECONOMICS REPORTER

The Globe and Mail, December 14, 2017