In this article, Rob Carrick shares three misconceptions a significant number of Canadians have with respect to their personal financial rights and responsibilities. This lesson plan reviews these mistakes and highlights the importance of financial literacy.

Appropriate Subject Area(s):

Personal finance, banking, privacy.

Key Questions to Explore:

- What are the three common financial mistakes highlighted in this article/survey?

- How can these mistakes be avoided?

- What is Financial Consumer Agency of Canada’s mandate?

- Which educational tools can Canadians independently utilize to increase their financial literacy outside the classroom?

New Terminology:

Financial Illiteracy, PIN, Financial Consumer Agency of Canada (FCAC), mortgage.

- Financial illiteracy: Financial illiteracy is an inability to understand how money works in the world: how someone manages to earn or make it, how that person manages it, how he/she invests it (turn it into more) and how that person donates it to help others.

- PIN: A personal identification number is a numeric password used to authenticate a user to a system.

- FCAC: The Financial Consumer Agency of Canada (FCAC) ensures federally regulated financial entities comply with consumer protection measures, promotes financial education and raises consumers’ awareness of their rights and responsibilities.

- Mortgage: A mortgage is a loan used by purchasers property to buy real estate.

Materials Needed:

- A copy of the article.

- A copy of the survey: https://www.canada.ca/content/dam/fcac-acfc/documents/programs/research-surveys-studies-reports/financial-consumers-rights-responsibilities-2016.pdf

Introduction to lesson and task:

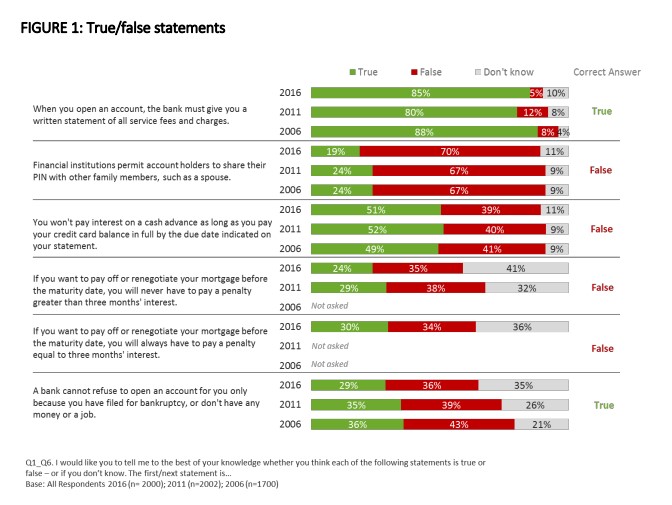

The financial consumer’s rights and responsibility (a 2016 report prepared by IPSOS Public Affairs Canada for the Financial Consumer Agency of Canada) found that a significant number of Canadians lack awareness about basic PIN rules (30%), cash advance rules (61%), and mortgage rules (65%). Given the usage rate of debit cards, credit cards, and mortgages, a general lack of awareness about these products could lead to misuse, which often comes with high costs.

The graph below provides comparable information from prior years. Benchmarking 2016 results against 2011 shows that financial literacy has seen a slight improvement in Canada. There has been a3 percentage point increase in the proportion of Canadians who know that financial institutions do not permit sharing PIN information with anyone, including family members. Unfortunately, there has been a slight decrease (1point) in the number of Canadians who know that that interest on cash advances from a credit card begins to accrue immediately. Finally, Canadians appear to be more uncertain about mortgage prepayment penalty rules.

This lesson plan will seek to explore the impacts of all three misconceptions and provide tips on how students can improve their personal finance knowledge.

- Sharing PIN number with family members: Sharing PIN number with others leaves individuals more prone to unauthorized access which could lead to loss of funds, property or identity theft. In addition, by sharing such personal information, individuals inadvertently nullify their personal banking security guarantee, leaving them ineligible for reimbursement in the event they suffer losses to their accounts. Students should be advised to keep their PIN number confidential.

- Cash advance: Cash advances cost a processing fee of $3.50 and the interest is charged from the day the transaction is made; occasionally at a high rate of 21.99%. Students should be advised that cash advances from a credit card should serve as a last resort for borrowing because they are typically very expensive. If a cash advance is used, it should be paid as soon as possible, to avoid incurring high interest expenses.

- Mortgage payments: Occasionally people may wish to pay off their mortgage before the term of the mortgage is over, typically because they wish to avoid future interest payments or future obligations or because they have the cash available. However, it is advisable to understand the costs of early payments and more effective means through which capital can be allocated.

In this FCAC survey, almost 25% of the participants believe that the maximum penalty for breaking a mortgage is capped at three months’ interest. In reality, the penalty is set at the higher of three months’ interest or a calculation called interest rate differential. Therefore, the minimum penalty is equivalent to three months of interest.

These misconceptions highlight the importance of financial literacy. A lack of financial literacy affects an individual’s ability make optimal financial decisions. If Canadians can increase their financial literacy, we could see a reduction in household debt levels and increased saving and investing.

It is also important to inform your students about the FCAC and its function. The Financial Consumer Agency of Canada (FCAC) ensures federally-regulated financial entities comply with consumer protection measures, promotes financial education and raises consumers’ awareness of their rights and responsibilities.

Financial literacy is all about knowing one’s financial rights and responsibilities, making informed decisions, and managing one’s financial affairs confidently.

While a $3.50 processing fee and interest rate on a cash advance may seem like a small price to pay, as transactions mount the impact of imprudent transactions becomes more severe. It is important to let your students know that it all adds up, eventually. Students should focus on increasing their knowledge of financial products and exercising financial discipline to utilize them in the right way.

There are also numerous avenues through which your students can improve their personal finance knowledge. The following are potential avenues available outside the classroom: personal finance news columns, personal finance websites like cfee.org, attending financial literacy conferences, etc.

Action (lesson plan and task):

Ask all the questions, and gauge responses.

- Conduct the survey in your own classroom by asking the following questions:

To the best of your knowledge indicate whether you think each of the following statements is true or false – or if you don’t know:

- A bank cannot refuse to open an account for you only because you have filed for bankruptcy, or don’t have any money or a job.

- When you open an account, the bank must give you a written statement of all service fees and charges.

- You won’t pay interest on a cash advance as long as you pay your credit card balance in full by the due date indicated on your statement.

- Financial institutions permit account holders to share their PIN with other family members, such as a spouse.

- If you want to pay off or renegotiate your mortgage before the maturity date, you will always have to pay a penalty equal to three months’ interest.

- If you want to pay off or renegotiate your mortgage before the maturity date, you will never have to pay a penalty greater than three months’ interest.

- Ask your students to state the three common mistakes Canadians make with respect to their personal finances

- Ask your students to state the function of the Financial Consumer Agency of Canada (FCAC).

- Ask your students to explain why it is not recommended to share their PIN with their family members.

- Ask your students to explain why cash advances should be the last resort when it comes to borrowing.

- Ask your students to explain why the penalty to pay off a mortgage may be more than three months’ worth of interest.

- Ask your students to share some of their prior personal finance misconceptions with the class and how they corrected their mistakes.

- Ask your students to state the potential costs of personal finance misunderstandings.

- Ask your students to explain how they increase their personal finance knowledge outside the classroom.

Consolidation of Learning:

- Share the correct answer to the survey with your students and let them know how well they performed, in comparison to the findings of the Ipsos survey.

- Ask your students to indicate the tools they utilize to increase their financial literacy knowledge outside the classroom?

Success Criteria:

- After completing this lesson plan, students should be able to avoid these three common mistakes. And they should become aware of materials available to increase their personal finance knowledge.

Confirming Activity:

- Ask your students to explain why it is important to have a solid understanding of personal finance concepts.