Exclusive data show house prices are at the core of Canada’s growing debt burden, reports Tamsin McMahon

Policy-makers have long warned that Canada’s booming housing market has a dark side: an extended run-up in household debt.

Trying to shed some light on the growing debt burden, The Globe and Mail analyzed data provided by Equifax Canada on average debt for more than 450,000 postal codes covering every region of the country from 2013 to 2015.

The data show that neighbourhoods where household debt is the highest and has risen the most tend to be home to the country’s most expensive real estate, as well as parts of Alberta that have seen an influx of young, first-time buyers. Meanwhile, households in Atlantic Canada, where home prices are among the lowest in the country, have the highest consumer debt balances.

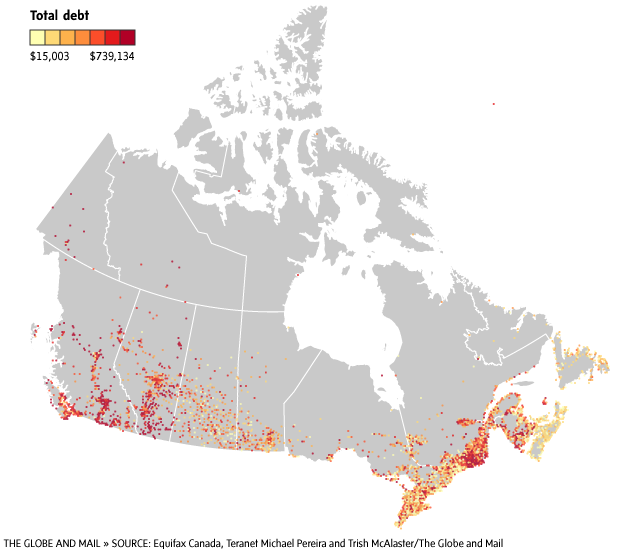

High debt

Nationally, debt averaged more than $44,000 in the third quarter of 2015, up 22 per cent from two years earlier. More than 1,200 postal codes, representing 41,000 households, had average debt of more than $200,000 last year.

Not surprisingly, high-debt postal codes tended to be in areas with the highest home prices. In Vancouver, that includes much of the west side of the city, neighbourhoods such as Kitsilano, West Point Grey and Kerrisdale, where average home prices can top $3-million. High-debt neighbourhoods also clustered in affluent suburbs such as West and North Vancouver, as well as pockets of White Rock and Richmond.

Debt also followed home prices in the Greater Toronto Area, clustering in neighbourhoods such as Forest Hill, Moore Park and Leaside and affluent enclaves in suburbs such as Richmond Hill and Oakville. In Calgary, high-debt neighbourhoods tended to be in the city centre and in expensive subdivisions such as Aspen Woods.

Alberta is the outlier

Thanks to what was until recently Canada’s strongest job market, Alberta has seen an influx of young workers, many of whom became first-time buyers, helping to fuel the province’s housing market and its household debt burden.

That helps to explain why even though home prices in the province are lower than the national average, many neighbourhoods in Calgary, Edmonton and Fort McMurray rival the most expensive areas of Toronto and Vancouver when it comes to debt.

Over all, Albertans owed an average of more than $57,000 in the third quarter of last year, according to Equifax data, up 32 per cent from 2013 and nearly 30 per cent above the national average.

The province is home to more than its share of high-debt households. More than 400 postal codes, corresponding to roughly 18,000 households, had debt averaging above $200,000 in the third quarter of last year. That compared with 11,000 B.C. households, even though average home prices were twice as expensive in British Columbia.

Of those high-debt Albertan households, more than half were concentrated in just four places: pockets of Fort McMurray, Northwest Calgary, Southeast Calgary and Southwest Edmonton that have all seen a spate of new home building in recent years.

Thankfully, Albertans have been able to tolerate their high debt because they have some of the highest incomes in Canada and, until oil prices collapsed 18 months ago, some of the country’s lowest unemployment rates.

But analysts have been paying particularly close attention to the province’s deteriorating economy, given that the large debt loads and high home prices could make it difficult for Albertans to tap into their home equity to weather the economic storm, while businesses may have trouble leaning on indebted consumers to spend their way out of the downturn.

A tale of two markets

Statistically speaking, the neighbourhoods of Timberlea in North Fort McMurray and West Vancouver’s British Properties look roughly the same when it comes to household debt. Both are among Canada’s most-indebted regions, with about 12 per cent of residents living in neighbourhoods where the household debt averages more than $200,000 and debt in some neighbourhoods approaches $500,000. Both are also among the most highly sought-after and expensive neighbourhoods in their respective communities. But that’s where the similarities end.

At the centre of Canada’s oil economy, sprawling Timberlea is home to one of the country’s youngest, wealthiest and fastest-growing populations.

Median household incomes in the neighbourhood topped $200,000 in 2013, according to Statistics Canada. More than half of the residents had moved to Fort McMurray from other parts of the country. Many are young families. Children under the age of 15 made up one-fifth of the neighbourhood’s population in the most recent census.

At an average of $626,000 as of January, according to data from National Bank and Teranet, homes in Timberlea are among the most expensive in Fort McMurray.

That has made it one of the places that has been hardest hit by job losses in the oil patch, and devastating wildfires now are sweeping through the community. (Data on both household debt and home prices predate the wildfires, which have damaged some homes in Timberlea, but kept the majority intact.)

By March, median detached home prices had dropped more than 7.5 per cent from a year ago to $657,500, according to the Fort McMurray Real Estate Board, while condominium prices have dropped 34 per cent.

By contrast, the exclusive British Properties community has been the centre of a very different economic phenomenon: the insatiable appetite for Vancouver real estate.

Compared with people in Timberlea, residents of British Properties are more likely to be older and immigrants and less likely to be employed or to have young children living at home. The median income in 2013 was just $85,000, well below what would be considered necessary to afford the community’s home prices, which have risen by an annualized 31 per cent, to an average of more than $3.6-million.

Despite the dramatic difference in the price of homes and incomes in the two neighbourhoods, it is actually high-earning Timberlea that was home to the highest-debt neighbourhood last year. In a stretch of homes within a new subdivision along Dafoe Way and Dixon Road, homes sell for around $700,000, while average debt topped $500,000.

That compared with a maximum average debt balance of $438,000 in British Properties’ most-indebted postal code, a group of homes along Eyremount Drive, where prices can reach $12-million.

Low debt

Canada’s major cities are home to neighbourhoods with both the highest and lowest debt, a reflection of the fact that they are a magnet both for the country’s wealthiest home buyers and for low-income residents relying on affordable rental housing.

Low-income, low-debt neighbourhoods can be found in the downtown cores of major cities and along major thoroughfares, such as Toronto’s Yonge Street, Vancouver’s Downtown East Side and Winnipeg’s North End. In postal codes where average household debt was below $1,000, home prices averaged $350,000 in the last census, compared with $840,000 in neighbourhoods with average debt above $200,000.

In many cases, however, low-debt households live side by side with high-debt ones.

In Toronto’s upscale Lawrence Park neighbourhood, for instance, low-debt postal codes cluster along the Yonge Street corridor, home to businesses, condos and mixed-use rental apartments, while high-debt postal codes tended to line the residential side streets.

Meanwhile, in Calgary’s Evanston neighbourhood, high-debt postal codes cluster in areas of recently built homes, while more established areas generally have lower debt.

City versus suburb

In an unexpected twist, given the soaring price of real estate in Canadian cities, debt actually tend to be higher on average in the suburbs than the large cities that they surround.

Nationally, household debt in the six largest cities averaged $46,500 in the third quarter of last year, while home prices averaged $568,000. In the suburbs, however, average debt topped $53,000, while home prices averaged $527,000. (The relatively high suburban home prices are skewed in part by Metro Vancouver, home to expensive suburban communities such as West Vancouver.)

Nearly half of all neighbourhoods in suburbs around Canada’s six largest cities had debt of more than $50,000 compared with a third of neighbourhoods in the cities.

The debt divide between the cities and their suburbs is a story of extremes: Cities are home to significant concentrations of high-income, high-debt neighbourhoods, but also to a large number of low-debt, low-income communities, students and other renters.

Suburbs tend to have less variety of very rich and very poor, although their lower home prices also make them attractive to younger first-time home buyers.

In the Greater Toronto Area, for instance, the city of Toronto was home to three times as many neighbourhoods with average debt above $200,000 than the surrounding suburb communities. At the same time, nearly a quarter of Toronto neighbourhoods had less than $20,000 in household debt on average, compared with just 8 per cent of suburban neighbourhoods.

Metro Vancouver’s most highly indebted postal code was a collection of homes along Braeside Drive, where properties sell for $1.5-million to $3.5-million and debt averaged nearly $740,000. By comparison, in the most-indebted neighbourhood in Vancouver itself, a postal code in Shaughnessy, debt averaged $685,000 while homes typically sell for more than $10-million.

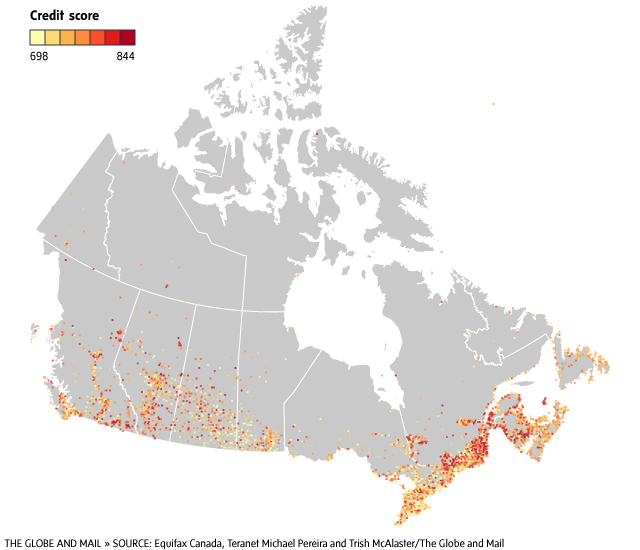

Credit scores

When lenders want to assess a borrower’s risk of defaulting on a loan, they turn to credit scores: personalized measures based on an individual’s debt levels, access to credit and repayment history.

Credit scores vary widely in Canada, from an average low of 434 in a neighbourhood in Thunder Bay to a high of 831 in the Westwind neighbourhood of Richmond, B.C., although more than 70 per cent of Canadians had scores above 720, a measure considered by lenders to be “superprime” or excellent.

Credit scores often follow affluence and home prices. Very high credit scores tend to be concentrated in wealthy neighbourhoods of the largest cities and their suburbs.

“Near prime” and “subprime” borrowers, those with credit scores below 660, were found in the downtown cores of major cities, along with smaller places such as Prince George, B.C., Grand Prairie, Alta., and downtown Hamilton.

Large segments of Vancouver’s western neighbourhoods and West Vancouver had credit scores that qualified them as superprime borrowers, as did much many neighbourhoods the central core of Toronto and the suburbs that line the lakefront to the west.

By contrast, more than 40 per cent of postal codes in Winnipeg’s north end and in uptown Saint John had credit scores that fell below the level considered to be a “prime” borrower.

Neighbourhoods with lower credit scores typically have lower debt than those with very good credit. Fort McMurray’s Timberlea was the exception once more, a neighbourhood where about a third of homeowners had both high debt and credit scores below a level that some financial institutions would consider excellent.

Non-housing debt

Unlike mortgages, consumer debt that is not tied to the value of real estate tends to be highest in areas where home prices have not soared in recent years.

The highest concentration of consumer debt loads can be found in Atlantic Canada, particularly New Brunswick, Nova Scotia and rural parts of Newfoundland. In the community of Paradise, Nfld., for instance, a quarter of neighbourhoods had consumer debt of more than $20,000 in the third quarter of 2015, compared with less than 1 per cent of postal codes in Calgary’s Deer Park neighbourhood.

The largest driver of high consumer debt appears to be low housing-related debt. Mortgages made up just 60 per cent of total household debt in some areas of New Brunswick’s Acadian Peninsula, compared with as much as 85 per cent in some neighbourhoods of Vancouver.

Home-equity lines of credit also tended to be concentrated in regions where home prices were high, such as the core of Toronto and the west side of Vancouver. Meanwhile, only a handful of neighbourhoods in Atlantic Canada carried average balances of more than $30,000 on lines of credit secured by their homes.

How we did the analysis

The analysis based is based on household debt data provided to The Globe by Equifax Canada. The postal-code-level data included average balances of mortgage debt, home-equity lines of credit and consumer credit not tied to housing, along with Equifax’s average credit score for the postal code. The data are tied to individual consumers, rather than to properties, and also include some debt data on small businesses.

Even at the postal-code level, neighbourhoods are often a patchwork of vastly different households, each with its own unique financial situation. For instance, fewer than 40 per cent of Canadians actually have a mortgage, with the remaining 60 per cent split between renters and mortgage-free homeowners. Average debt levels can obscure such variety.

The analysis also does not take into account household assets and incomes, which in many high-debt neighbourhoods can be considerable.

TAMSIN MCMAHON

The Globe and Mail Last updated: Wednesday, Jun. 01, 2016 9:21AM EDT