Canadians’ wallets are feeling the bite on two sides: soaring prices and rising borrowing costs. We crunched the numbers to show how much more they’re paying.

The financial double bite is everywhere. A stick of margarine costs 50 per cent more than it did two years ago. Advertised rents are, on average, about $100 a month above where they were in 2019, already an extraordinarily expensive year to be a new tenant. And, even with fixed mortgage rates, homeowners will likely see their monthly payments rise by hundreds of dollars if they’re up for first-time renewals in the next few months.

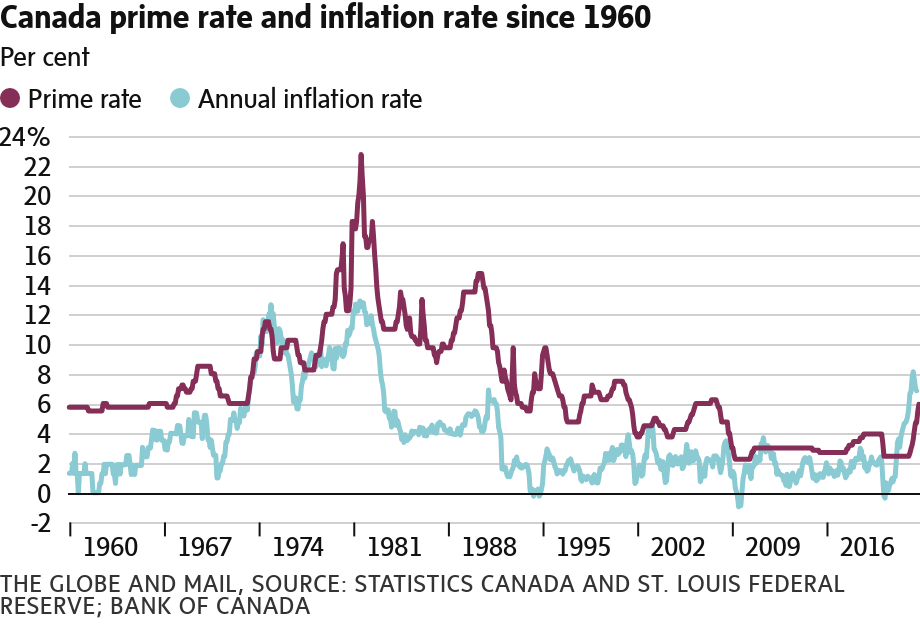

In Canada – as in the U.S., Europe and many other parts of the world – people’s budgets are being devoured from two directions at once. On one side of the bite are higher interest rates, which increase borrowing costs throughout the economy. On the other side is inflation, which has been running at multi-decade highs.

Central banks are pushing interest rates higher to force consumers and businesses to rein in spending and borrowing, which would in turn cool the economy and slow down the pace of price increases. But achieving that end result will take time.

And so for now inflation remains high, even though the Bank of Canada has cranked its trendsetting interest rate up to 3.75 per cent, the highest level since 2008. While payments on mortgages and other types of loans are already getting higher, the supposed benefit of those increased borrowing costs – slower price increases on groceries and other essentials – has yet to materialize.

So how much more are Canadians paying just to get by these days? The impact of inflation and interest rates varies significantly depending on spending habits, debt loads and household income, with lower-earning Canadians struggling the most. Still, some simple math makes it easier to grasp the size of the financial double-hit.

Here are six examples that help quantify the bite.

Groceries

The cost of feeding a family of four was $265 per week in 2021, according to a national estimate by Canada’s Food Price Report, which provides an annual gauge of food-price trends. Adjusting that for inflation suggests the weekly spend now stands at $296, roughly $30 higher than in 2021 and $40 higher than in 2020. The erosion of purchasing power is significant. At 2020 prices, someone would now be able to buy just 80 per cent of an apple, a chicken or a can of pop, data from Statistics Canada show. It’s an especially heavy hit for lower-income families, who spend more of their disposable income on essentials than wealthier households.

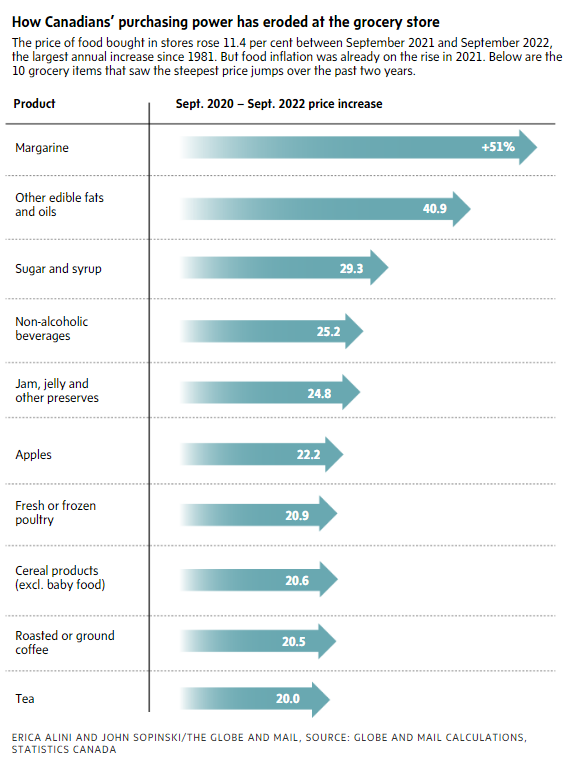

And food inflation has continued to pick up speed despite lower transportation costs and fewer supply chain bottlenecks. The price of food bought in stores was up 11.4 per cent in September compared to the same month in 2021, the largest annual increase since 1981.

Gas

Driving isn’t cheap, either. Sure, gasoline prices have come off the summer’s record highs, which is a major reason overall inflation dipped to 6.9 per cent in September, down from a peak of 8.1 per cent in June. But filling the 50-litre tank of a Toyota Corolla still cost $13 more toward the end of October than it did this time last year, according to national average gas prices provided by CAA. If you drive a truck or large SUV, the difference is closer to $20.

Mortgages

Mortgage payments are another massive squeeze on many household budgets. For homeowners with variable mortgage rates and fluctuating payments, every quarter of a percentage point increase in interest rates translates into an additional $14 a month for every $100,000 of outstanding mortgage, according to Victor Tran, a mortgage and real estate expert at Ratesdotca, a financial products comparison website.

On a mortgage of that kind with a balance of $380,000 – roughly the average borrowed by first-time homebuyers over the past two or so years – rate hikes since March have increased payments by almost $745 a month.

And while eight out of 10 Canadians with variable-rate mortgages have fixed payments, which usually insulate them from some of the effects of rising interest rates, many of them are also seeing their monthly costs swell. As interest rates spike, many of these borrowers are starting to reach their so-called “trigger points,” at which their monthly payments no longer cover the interest owed. That threshold typically prompts lenders to demand bigger payments, unless mortgage holders can make lump-sum contributions toward their principal.

Many Canadians with fixed-rate mortgages aren’t sleeping easy either. The share of outstanding mortgages coming up for renewal this year is significantly lower than usual, because borrowers rushed to refinance their existing mortgages earlier in the pandemic to lock in record-low interest rates, said Ben Rabidoux, founder of North Cove Advisors, a market research firm.

But homeowners who didn’t refinance and are coming up for their first renewals are facing considerably larger payments, he warned. For example, those who bought in 2017 and are renewing five-year fixed rates are seeing monthly payments rise by roughly $100 for every $100,000 outstanding, Mr. Rabidoux said.

And while lofty borrowing costs have put a damper on the housing market, home price declines so far have done little to offset the impact of rising rates on new homebuyers. As of the end of June, for example, the average amount borrowed by first-time buyers had shrunk by just 0.5 per cent compared to the first three months of the year, while their average monthly payments had climbed by 10 per cent, according to Equifax, one of Canada’s two major credit bureaus.

Lines of credit

Canadians with outstanding balances on their lines of credit, which have variable interest rates, are also feeling the heat. For example, consider someone with a home equity line of credit (HELOC), which uses a borrower’s home as collateral. Suppose this homeowner had an outstanding balance of $67,000, in line with the average Canadians owe on HELOCs, according to the latest available data from Equifax. With an interest rate of 2.35 per cent – the lowest nationally available in October, 2021, according to financial products comparisons site Ratehub.ca – this borrower would have had an interest-only minimum payment of $131 a month.

Now, a year later, that borrower is paying $327 a month, at an interest rate of 5.85 per cent, assuming their lender adjusted rates in lockstep with the Bank of Canada. That’s a difference of $200 a month, on a payment that makes no dent in the principal amount.

Many students and recent graduates are also facing a formidable cash crunch. Ottawa has frozen the accrual of interest on the federal portion of Canada Student Loans until the end of March, and has promised to eliminate that interest entirely starting in April. But borrowing costs are ticking up on student lines of credit. The burden is especially heavy for professional-degree students, such as lawyers, doctors and veterinarians, who often leave school with six-figure balances.

For example, the interest-only payment on a student line of credit with a $100,000 balance and an interest rate of 2.7 per cent would be $225 per month. But, after the recent slew of central bank rate increases, that borrowing rate would be 6.2 per cent, which would come with a minimum payment of around $517. Students must pay at least the interest on their lines of credit – which are provided by financial institutions – even while they’re in school. After graduation, and often after grace periods of up to a year, borrowers must begin to make payments that include both principal and interest.

Rent

At the other end of the financial bite, rent inflation is also disproportionately ravaging the finances of students and younger workers, along with those of many lower-income Canadians. The average asking rent for all properties posted on the website Rentals.ca was $2,043 per month in September, up 15 per cent from a year ago and more than $100 higher than the pre-pandemic peak in 2019.

While rising interest rates usually put downward pressure on inflation, experts say they’ve had the opposite effect on Canada’s rent inflation so far. Although interest rates don’t affect tenants directly, higher borrowing costs are forcing some priced-out would-be homebuyers to keep on renting. This is adding to soaring demand for rental housing among international students, new immigrants and workers returning to offices.

Auto Loans

Another uncommon interaction between inflation and borrowing may soon play out in the auto loan market, said Rebecca Oakes, vice-president of advanced analytics at Equifax Canada. Prices for both new and second-hand cars and light trucks spiked to record highs as auto manufacturers struggled to meet consumer demand among persistent supply chain snarls. That, in turn, has been driving up auto loan balances, with payments for new-vehicle buyers averaging $770 a month so far this year, up from $715 last year and $685 two years ago, according to research firm J.D. Power. The trend has also resulted in more Canadians opting for longer loan terms of seven or eight years to finance their vehicle purchases, according to Ms. Oakes.

Those large balances and longer loans may become particularly painful for people who bought used vehicles, she added. As supply chain logjams ease, the resale values of second-hand cars might drop unusually steeply, “and then you’re going to have consumers with potentially a loan that is way above the value of the vehicle,” she said.

How long the dual-sided attack on Canadians’ budgets will last is an open question. The Bank of Canada signalled at the end of October that the current cycle of interest-rate hikes is likely nearing its end. As higher borrowing costs percolate through the economy, the pace of price increases generally decelerates, which, in turn, usually leads interest rates to decline. But Canada’s central bank doesn’t see inflation returning to its pre-pandemic normal until the end of 2024, and some economists fear the process could take far longer.

“When inflation has previously gone to levels as high as it is right now, it’s usually been slow to drift lower again,” a recent note by economists at Deutsche Bank warned. Their research shows that, historically, after spikes in the inflation rate, price increases were still above the pre-shock rate five years later.

For consumers, a longer fight against inflation would only drag out the double bite.

ERICA ALINI

The Globe and Mail, November 4, 2022